venividivicibj

Stylish Dinosaur

- Joined

- Apr 9, 2013

- Messages

- 22,869

- Reaction score

- 18,389

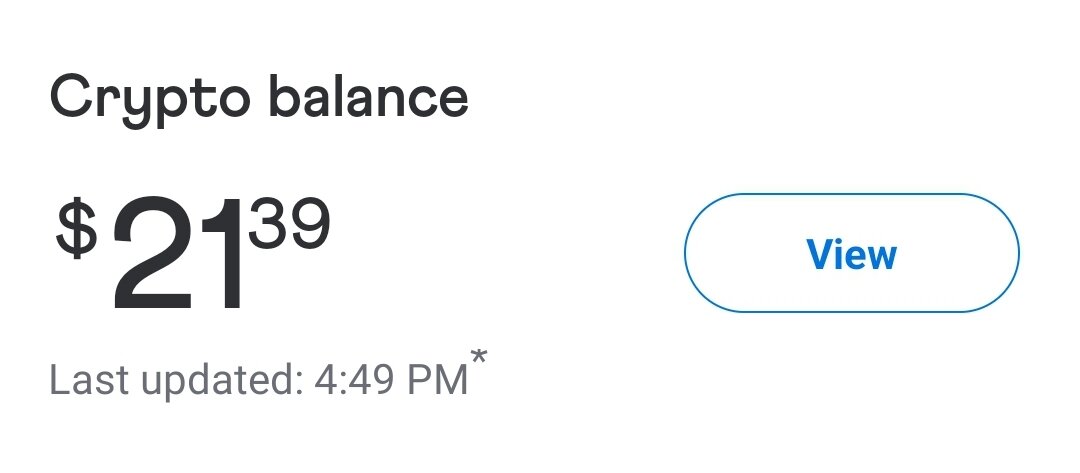

I think the people pushing hardest on crypto haven't admitted that the gains have been illogical and are due for a correction. There were some generic "well, sure it could drop, but it is going to keep going up in the long term."

: ( I’ve been saying we were due for a correction for a while