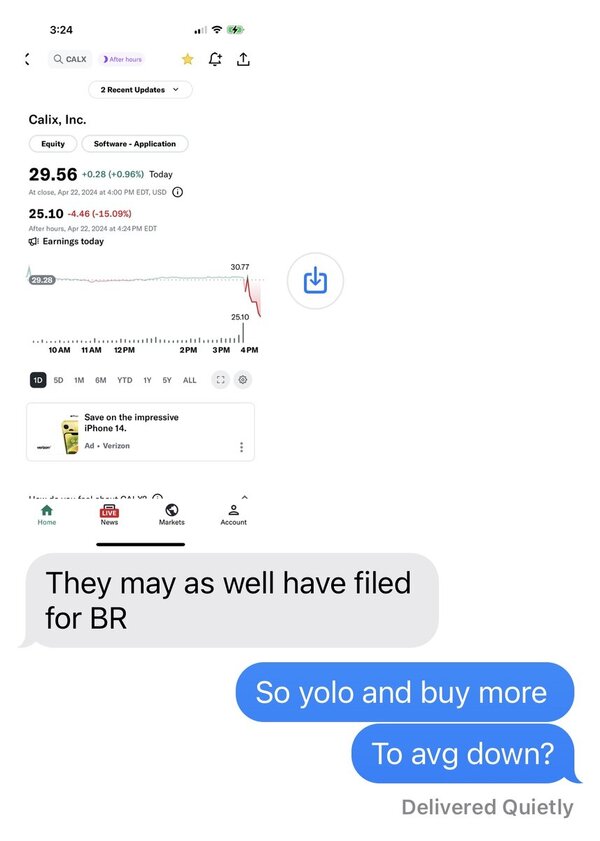

Too small a sample yet, but I'm (in simulation) up about 3.2% on SPY and 10% on UPRO since Oct 24th. The Market is up by less than 1% since then. Also today is looking good. Long yesterday, made some fake money, short today, hopefully this holds.

-

Hi, I am the owner and main administrator of Styleforum. If you find the forum useful and fun, please help support it by buying through the posted links on the forum. Our main, very popular sales thread, where the latest and best sales are listed, are posted HERE

Purchases made through some of our links earns a commission for the forum and allows us to do the work of maintaining and improving it. Finally, thanks for being a part of this community. We realize that there are many choices today on the internet, and we have all of you to thank for making Styleforum the foremost destination for discussions of menswear. -

This site contains affiliate links for which Styleforum may be compensated.

-

UNIFORM LA Japanese BDU Camo Cargo Pants Drop, going on right now.

Uniform LA's Japanese BDU Camo Cargo Pants are now live. These cargos are based off vintage US Army BDU (Battle Dress Uniform) cargos. They're made of a premium 13.5-ounce Japanese twill that has been sulfur dyed for a vintage look. Every detail has been carried over from the inspiration and elevated. Available in two colorways, tundra and woodland. Please find them here

Good luck!.

-

STYLE. COMMUNITY. GREAT CLOTHING.

Bored of counting likes on social networks? At Styleforum, you’ll find rousing discussions that go beyond strings of emojis.

Click Here to join Styleforum's thousands of style enthusiasts today!

Styleforum is supported in part by commission earning affiliate links sitewide. Please support us by using them. You may learn more here.

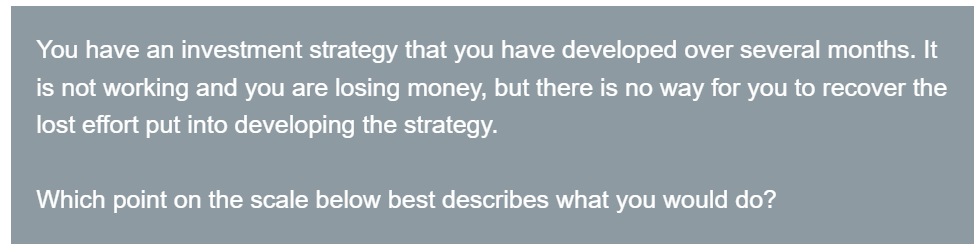

Talking stocks, trading, and investing in general

- Thread starter mikeman

- Start date

- Watchers 332

")

FEATURED PRODUCTS

-

Fornasetti Milano Limited Edition 15/97 Gold Inlay Burlwood Wood Valet Box As our friends at LuxeSwap primarily deal with textile garments, this exceedingly rare Fornasetti trinket box has to be special for them to work outside their normal wheelhouse - and it is. There are only 96 other examples of this limited edition box on the planet. Who knows when another one might ever surface for sale?

Fornasetti Milano Limited Edition 15/97 Gold Inlay Burlwood Wood Valet Box As our friends at LuxeSwap primarily deal with textile garments, this exceedingly rare Fornasetti trinket box has to be special for them to work outside their normal wheelhouse - and it is. There are only 96 other examples of this limited edition box on the planet. Who knows when another one might ever surface for sale? -

TLB Mallorca - Comfort Suede Loafers - $269 Designed for maximum comfort with lightweight rubber sole and supple leathers this model offers comfort all day long, as a perfect choice for the daily commute or casual outing. For this model, we have choosen suede leather in vivid colors, our sommelier last and a full rubber sole. It is also finished in blake construction.

TLB Mallorca - Comfort Suede Loafers - $269 Designed for maximum comfort with lightweight rubber sole and supple leathers this model offers comfort all day long, as a perfect choice for the daily commute or casual outing. For this model, we have choosen suede leather in vivid colors, our sommelier last and a full rubber sole. It is also finished in blake construction. -

UNIFORM/LA - Japanese Camo Cargo Pants - 248 USD Inspired by vintage US Army BDUs – the Japanese BDU Camo Cargo Pants are made of our ultra-premium 13.5-ounce Japanese twill and feature a perfect relaxed fit you’ll love. Outfitted with seven handy pockets throughout, these beautiful cargos feature premium waist cinching tabs with military webbing on the sides to ensure a secure fit.

Featured Sponsor

Forum Sponsors

- American Trench

- AMIDÉ HADELIN

- Archibald London

- The Armoury

- Arterton

- Besnard

- Canoe Club

- Capra Leather

- Carmina

- Cavour

- Crush Store

- De Bonne Facture

- Drinkwater's Cambridge

- Drop93

- eHABERDASHER

- Enzo Custom

- Epaulet

- Exquisite Trimmings

- Fils Unique

- Gentlemen's Footwear

- Giin

- Grant Stone

- House of Huntington

- IsuiT

- John Elliott

- Jonathan Abel

- Kent Wang

- Kirby Allison

- Larimars Clothing

- Lazy Sun

- LuxeSwap

- Luxire Custom Clothing

- Nicks Boots

- No Man Walks Alone

- Once a Day

- Passus shoes

- Proper Cloth

- SARTORIALE

- SEH Kelly

- Self Edge

- Shop the Finest

- Skoaktiebolaget

- Spier and MacKay

- Standard and Strange

- Bespoke Shoemaker Szuba

- Taylor Stitch

- TLB Mallorca

- UNI/FORM LA

- Vanda Fine Clothing

- Von Amper

- Wrong Weather

- Yeossal

- Zam Barrett

Members online

- CLH03

- New Shoes1

- KeepItClassy760

- jellyroller

- Ranjeev

- Newcomer

- barutanseijin

- terryleebrownjr

- _AMD

- Bidouleroux

- Close Horse

- kakishiboo

- Steves40th396

- shoppinglists

- Ortip

- ellsbebc

- Duke Silver

- wmvisvim

- bde

- William Kazak

- Fenderplyr

- BootsAndIndigo

- ramdomthought

- seanwolff

- UNIFORMLA

- Jr Mouse

- edinatlanta

- ogutierrez8310

- stook1

- hendrix

- mrs25962

- othertravel

- jcchvz2

- kevinftwman

- ilikethelights

- Redtop

- Omega Male

- brokencycle

- kritios

- kknybel

- up1911fan

- TinyEli

- ddohnggo

- workwear

- sartoria vacua

- zippyh

- ccpl14

- overtone

- lcdx22

- lagsun