- Joined

- Oct 16, 2006

- Messages

- 38,393

- Reaction score

- 13,643

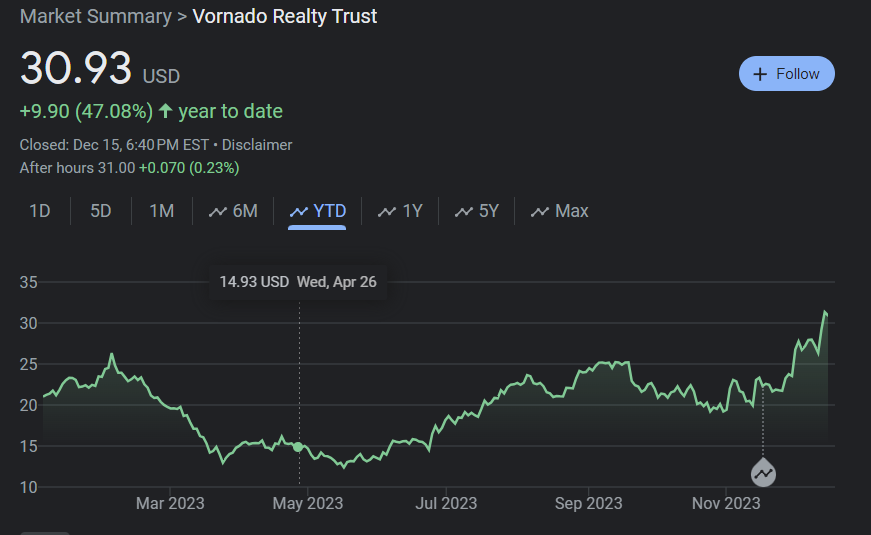

I just found out that shares awarded to me years back are now vested. Sell share. Buy shoes. BOOM.

STYLE. COMMUNITY. GREAT CLOTHING.

Bored of counting likes on social networks? At Styleforum, you’ll find rousing discussions that go beyond strings of emojis.

Click Here to join Styleforum's thousands of style enthusiasts today!

Styleforum is supported in part by commission earning affiliate links sitewide. Please support us by using them. You may learn more here.

Nicks Handmade Boots - BuilderPro® - ThurmanNW - $589

The BuilderPro® ThurmanNW is designed for those who demand ruggedness without compromising on comfort.

Nicks Handmade Boots - BuilderPro® - ThurmanNW - $589

The BuilderPro® ThurmanNW is designed for those who demand ruggedness without compromising on comfort.