Piobaire

Not left of center?

- Joined

- Dec 5, 2006

- Messages

- 81,814

- Reaction score

- 63,325

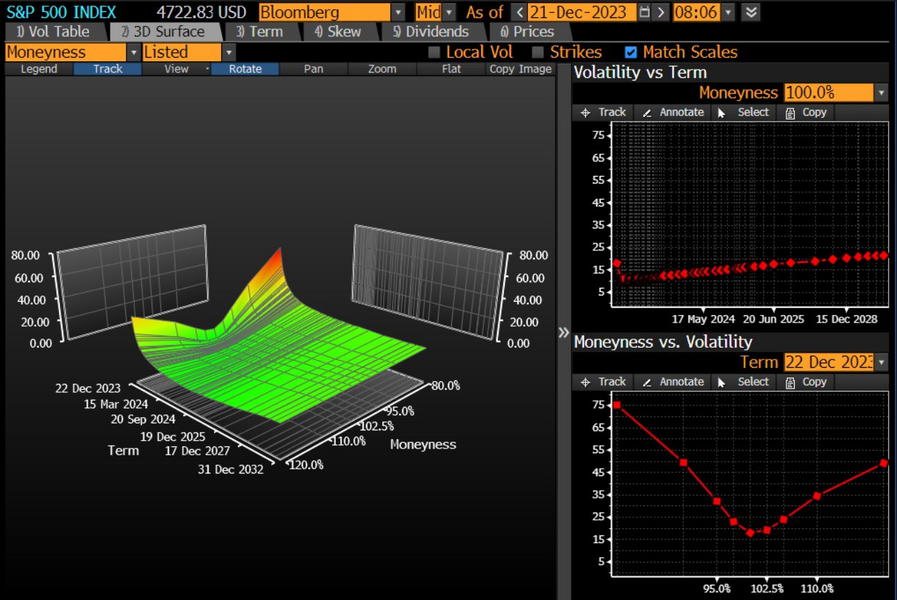

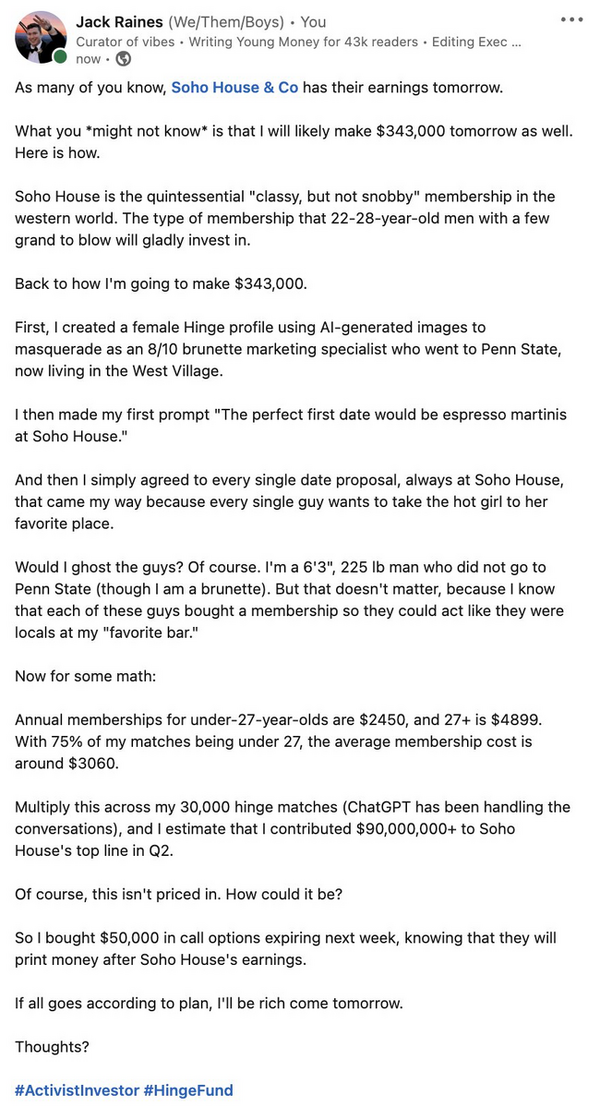

volatility baby!

Theta needs to burn off as I just opened the position yesterday. Delta is also involved as it's not like OTM 30 DTE options are going to be 1. Then of course how does gamma impact delta, right?

I've been doing my homework quite thoroughly.

")